2017年美国通过的《减税与就业法案》(Tax Cuts and Jobs Act)多项重要临时性税收减免措施于2025年到期,如果相关延续法案 ,现在的 "大而美法案" 未通过,可能会有以下税收变化:

-个人所得税:

该法案实施前美国个人所得税保留7档税率,多数税率有所下调,最高一档税率从39.6%下调至37%。若法案不延续,2025年后个人所得税税率可能会恢复到2017年之前的水平,即最高税率可能调回39.6%,其他各档税率也会相应调整,纳税人的税负将增加。

-企业所得税:

法案将企业所得税率从35%降至21%,废除替代性最低税。若法案不延续,企业所得税税率可能会回升至35%,并且可能恢复替代性最低税,企业税负将大幅增加。

-分红及股票分红税:

2017年税改法案对适用于大量小企业的穿透性税收规定,这些企业收入的20%将免于征税。对于股票分红等,如果减税法案不延续,一方面企业利润若因企业所得税增加而减少,分红可能会受影响;另一方面,穿透性税收优惠取消后,相关企业主在分红时可能面临更高的实际税负。

-利息收入税:

目前没有明确资料显示2017年税改法案对利息收入税有直接调整,但如果整体税收政策发生变化,政府为了增加财政收入,可能会调整利息收入税的相关政策,比如提高税率或减少相关税收优惠等,从而导致利息收入税税负增加。

“大而美法案”,除以上提到的条款外,该草案中还有以下一些减税相关条款:

-个人所得税方面:永久实施现行的个人所得税税率,包括最高税率37%,并对各税率级距进行通胀调整。永久实施标准扣除额的通胀调整,单身申报者为15,000美元,夫妻合并申报者为30,000美元,并计划在2025年至2028年期间,额外提高1,000美元(单身)或2,000美元(夫妻合并申报)扣除额。永久维持儿童税收抵免额为每名子女2,000美元,并于2025年至2028年期间提高至2,500美元。

-企业所得税方面:企业所得税的21% flat tax rate永久化,即维持企业所得税税率为21%,这是对2017年税改中企业所得税优惠政策的延续。

-遗产及赠与税方面:永久提高遗产及赠与税免税额至1,500万美元,并每年进行通胀调整。

-投资特定穿透型企业方面:调整相关收入门槛及引入新规定,并将扣除额从20%提高至22%。

-最低税负制方面:延长最低税负制免税额及其适用门槛的高额度。

可是,如果“大而美”法案通过,会增加美国目前的财政赤字。

美国宾夕法尼亚大学沃顿商学院预计,2025 - 2034财年间静态基本赤字增量约2.8万亿美元,考虑到经济动态调整后基本赤字增加3.2万亿美元。美国国会官方的联合税务委员会(JCT)预计,法案将在未来10年增加赤字3.7万亿美元。联邦预算责任委员会(CRFB)估计,基本赤字增加2.9万亿美元,考虑付息的赤字规模增加3.3万亿美元,如果将一些暂时性的豁免条款永久化,则未来10年赤字增量将达到5.2万亿美元。

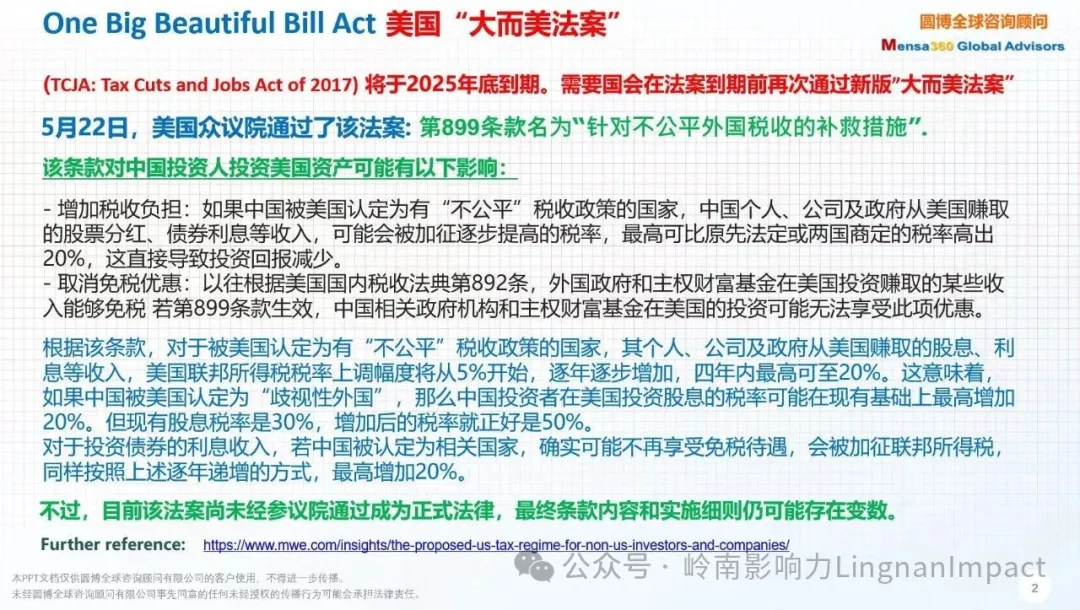

"大而美法案" 也加了 第899 条款,也许可能对中国投资人不利。分红从 30%加到50%, 利息从0% 加到20%。